audit working papers are the property of

The importance of working papers is as follows. The first statement is FALSE.

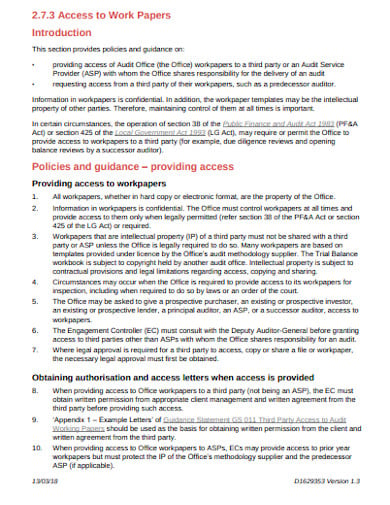

Audit Working Papers

Thus the working papers are the property of the auditor.

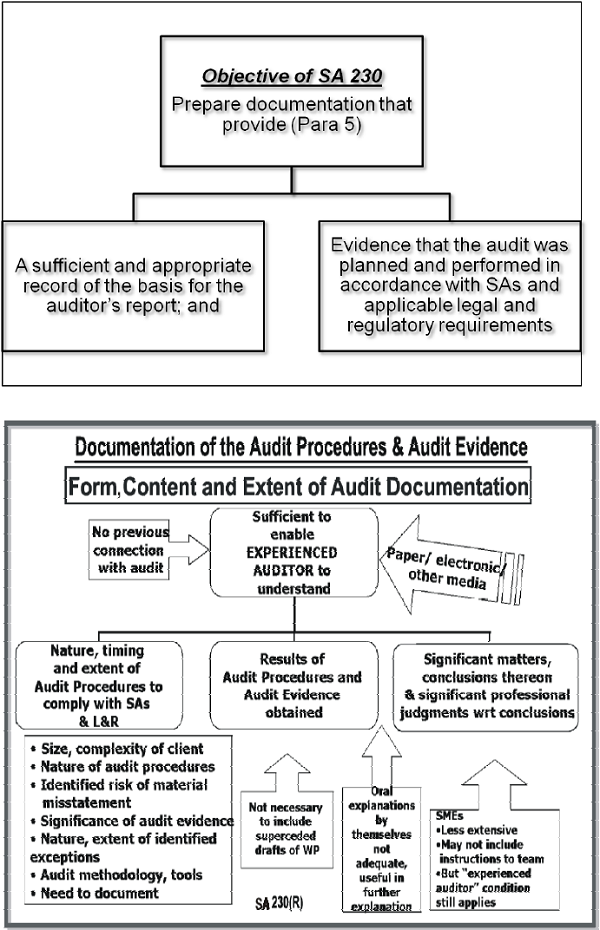

. Footnotes AU Section 339A Working Papers. Guidelines of Audit Working Papers as specified in SA-230 Audit Documentation. Audit working papers are the property of the auditors who may destroy the papers sell them or give them away Criticize this quotation.

The functions of audit working papers include. Aid in review of the work. Distort the papers sell them or give them to third part.

Working Papers prepared or obtained by the auditor in connection with the performance of audit are the property of auditor and it is the. This is essential because of the reason that audit working papers are used in order to create proper relevance when it comes to important matters pertaining to accounting and financial considerations of the company. Working Papers prepared or obtained by the auditor in connection with the performance of audit are the property of auditor and it is the duty of the auditor to retain and preserve the working papers for a period of 7 years.

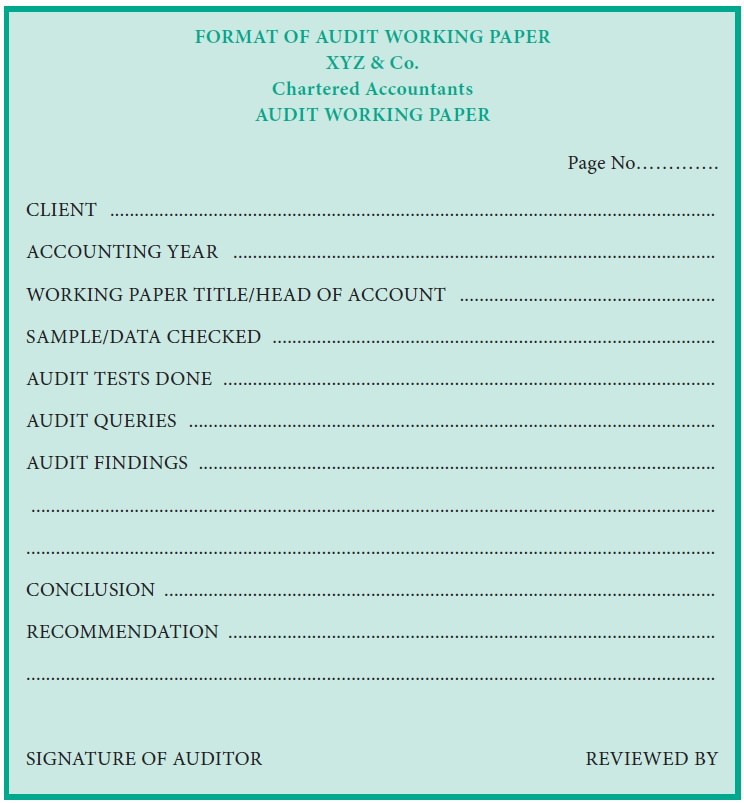

The auditors arrange the data properly in the working papers. Working papers are the record of various audit procedures performed audit evidence obtained allocation of work between audit team members etc. Audit working papers are used to document the information gathered during an audit.

In order to keep professional ethic it cannot discover to third party without consent of the client unless limited specified situations mentioned in ISA 230 Documentation and required by law the examples are court order for public interest and so on. The auditors rights of ownership however are subject to ethical limitations relating to the confidential relationship with clients. Working papers are the property of the auditor and some states have statutes that designate the auditor as the owner of the working papers.

Working papers also provide evidence that an audit was properly planned and supervised. Those documents include summarizing the clients nature of the business business process flow audit program or procedure documents or information obtained from the client and audit testing documents. Ownership of Audit working papers.

An audit programme is a set of _____ which are to be followed for properexecution of audit. Fn 2 This section does not modify the guidance in other Statements on Auditing Standards including the following. Audit programme helps in fixing the _____for the work done among the audit staffas work done may be traced back to the individual staff members.

Provide a means of assigning and coordinating audit work. Fn 1 This section amends section 230 Due Professional Care in the Performance of Work paragraph 04 by deleting the second sentence of that paragraph. A Audit working papers are the property of the auditors who may distort the papers sell them or give them to third part Is this statement true or false.

Record demonstrate the audit work from one tear to another. A review of the audit working papers gives an assurance that the audit work is both accurate and complete. Aid in the supervision review of the audit work.

Audit papers are the property of _____. They cannot distort them because it can be used as an evidence if there would be. So they are his property.

Document compliance with generally accepted auditing standards. She may at her discretion make portion or extracts from audit documentation available to the client c. Audit working papers are sometimes.

Audit documentation is the property of the client and sufficient and appropriate copies should be retained by the auditor for at least 5 years. Provide support for the auditors report. Audit working papers are the property of the auditor.

The Auditors Working Papers are divided into two parts. Audit working papers are the property of the auditors who may. Audit working papers are the property of the auditor.

Audit working papers are the documents and evidence that an auditor collects and retains with himself during the audit. Provide evidence of the audit work performed to support the auditors opinion. Hence the data become more meaningful and useful for the purpose of theaudit.

Subsequently question is for what minimum period should audit. Justify with your explanation. Working papers are necessary to corroborate the work and the findings of all the audit staff.

Audit working papers are the outcome of the documentation process. In order to keep professional ethic it cannot reveal to third parties without client consent unless limited specified situations mentioned in ISA 230 Documentation and required by law the examples are court order. List several rules to be observed in the preparation of working.

Although audit working papers are property of the auditors they should not be sold distorted or given to third party as it will violate the Code of Ethics of Confidentiality because what is contain in the audit working papers are information about the client. Is this statement true or false. Audit working papers also help in a.

Audit working papers are the property of the auditor. Plan the timing extent of audit procedures to be performed. Audit working papers refer to the documents prepared by or use by auditors as part of their works.

Of audit working papers as the supporting for the basis on which financial statement is approved by the auditor. If additional evidence is required to document significant findings or issues the original evidence is NOT considered sufficient and appropriate and should be deleted from the working papers d. The letter of audit inquiry to the clients lawyer required by.

Working paper is the property of the auditor. - a Client - b Accountant - c Auditor - d Registrar of companies - Advance Accounting and Auditing Multiple Choice Question-. Audit Working papers are without a doubt a very important part of the overall audit process.

They provide evidence that sufficient information was obtained by an auditor to support his or her opinion regarding the underlying financial statements. Which of the following statement is correct. Principles of Auditing Other Assurance Services 21st Edition Edit edition Solutions for Chapter 5 Problem 23RQ.

The working papers are the matters documented by the auditor. In order to keep professional ethic it cannot discover to third party without consent of the client unless limited specified situations mentioned in ISA 230 Documentation and required by law the. Although the client may claim them as a record of his business matters the auditor cannot part with them as his conclusions are based on them and as they provide evidence of the audit work carried out according to the.

Solved Answer of MCQ Audit working papers are the property of. Aid in planning performance of an audit.

Audit Working Papers

Audit Working Papers Types Characteristics Information

Guide To Standard On Auditing Sa 230 Audit Documentation

Audit Working Papers Meaning Definition Contents Objectives Importance Or Advantages Auditing

Working Papers In The Audit Process Definition Development Study Com

10 Audit Workpaper Templates In Pdf Word Free Premium Templates

Guide To Standard On Auditing Sa 230 Audit Documentation

10 Audit Workpaper Templates In Pdf Word Free Premium Templates

Audit Working Papers

Auditing And Accounting During And After The Covid 19 Crisis The Cpa Journal

2

10 Audit Workpaper Templates In Pdf Word Free Premium Templates

10 Audit Workpaper Templates In Pdf Word Free Premium Templates

Guide To Standard On Auditing Sa 230 Audit Documentation

Guide To Standard On Auditing Sa 230 Audit Documentation

Audit Working Papers Types Characteristics Information

Working Papers In The Audit Process Definition Development Study Com

Payroll Audit Working Papers Templates In Ms Excel Internal Audit Paper Template Audit

2